Who Cares About Climate Risk?

(The real estate sector should…)

When it comes to natural disasters, buildings, once constructed, are much like sitting ducks. But ducks can fly, and buildings cannot (as of yet). Climate events, including for example storms, heatwaves, and floods, thus pose a significant risk to buildings, whether commercial or residential. The recent sequence of superstorms (and subsequent flooding events) in major U.S. cities serves as a tangible reminder (think: New York, Houston, San Juan, PR, etc.). And it’s not just storms and flooding, but also cold spells, heat waves, drought, periods of extended precipitation, tidal flooding. Heat and flooding regularly account for the most weather-related deaths in the U.S., according to the National Weather Service. While such climate events already happen on a frequent basis, there is reason to believe that both the intensity and incidence will increase going forward. The New York City Panel on Climate Change, re-convened in the wake of Hurricane Sandy, projects an increase in the most intense hurricanes and increased precipitation from hurricanes.

For investors in real estate, be they shareholders of real estate investment trusts (REITs), direct investors in commercial real estate, or those investing through private equity firms, measuring exposure to climate risk often seems like a daunting task. However, the advent of (big) data has made climate risk analysis for real estate much more straightforward. On the one hand, maps of different types of climate risk are often publicly available. Although varying in detail and quality based on risk type and region, it is easy to access historical data on climate events, as well as forecasts of such events going forward (needless to say, a forecast is just that, and a high probability of an event occurring does not “guarantee” the event, think about earthquake risk in the San Francisco Bay Area). On the other hand, the location of real estate is fixed, and can be identified easily by a unique set of coordinates. Using the exact location of assets in an investment portfolio, investors can thus assess their exposure to flood risk, extreme temperatures, etc. with relative ease.

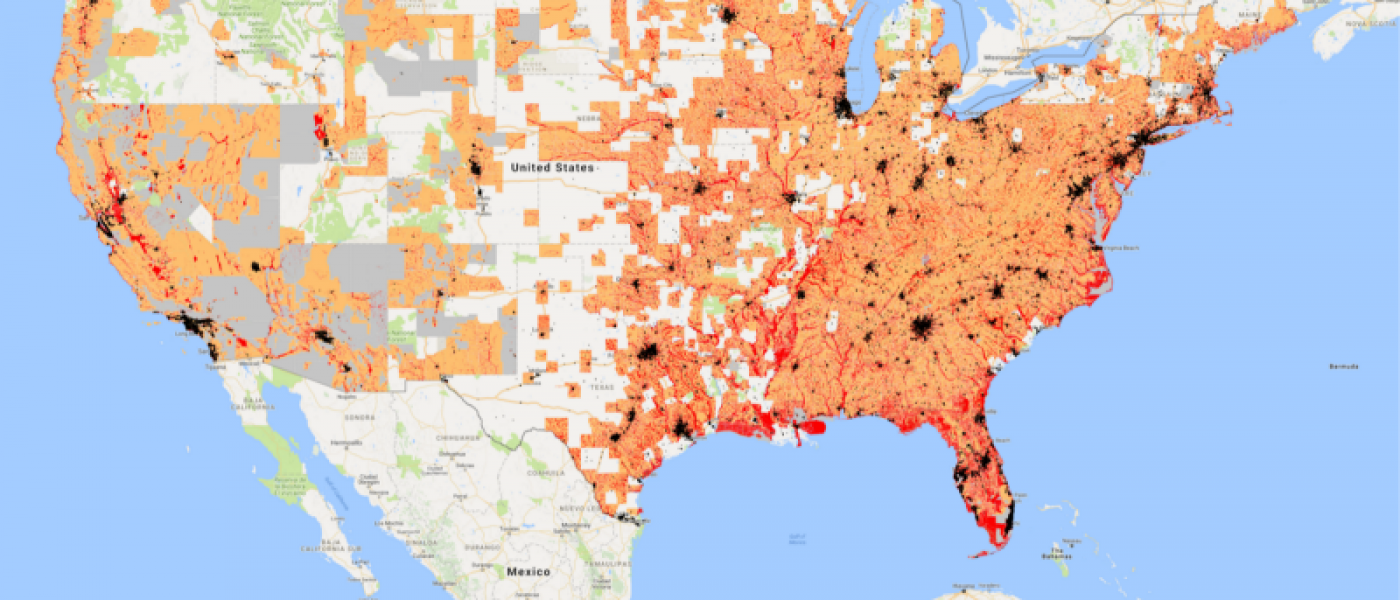

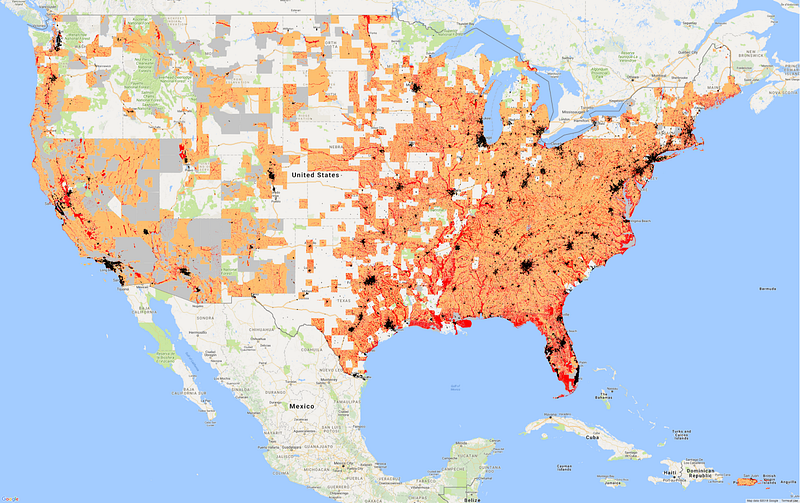

Using data collected by GeoPhy, we investigate all buildings held by 133 equity REITs with assets in the U.S. (some of these REITs are Canadian) as of Q1 2017. These portfolios, which represent just the U.S. holdings of these REITs, add up to a grand total of 36,641 buildings, covering almost 3.7 billion sq. ft. (3,709,107,064 sq. ft., to be precise). The maps below show the location of REIT assets and the overlay of two different climate risk layers. First, we use the well-known FEMA flood risk data — the Federal Emergency Management Agency (FEMA) uses their assessment of flood risk for federal insurance purposes. While often criticized for being inaccurate (either indicating “false positives” or “false negatives”), the FEMA flood risk data is used widely in the real estate market.

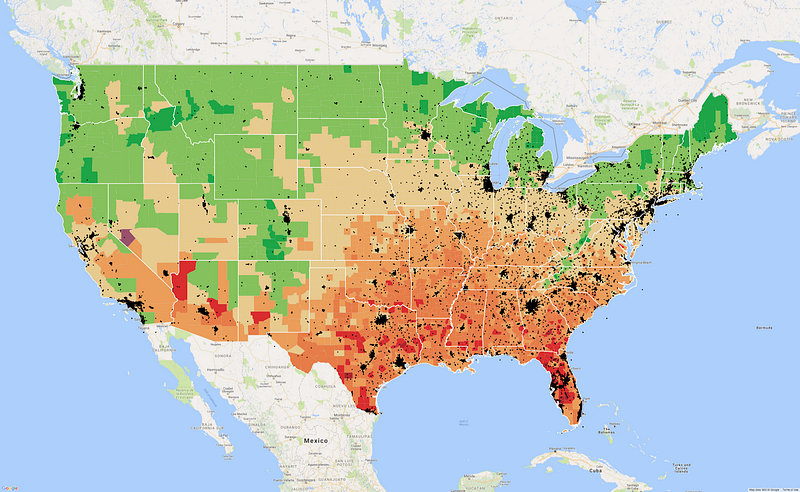

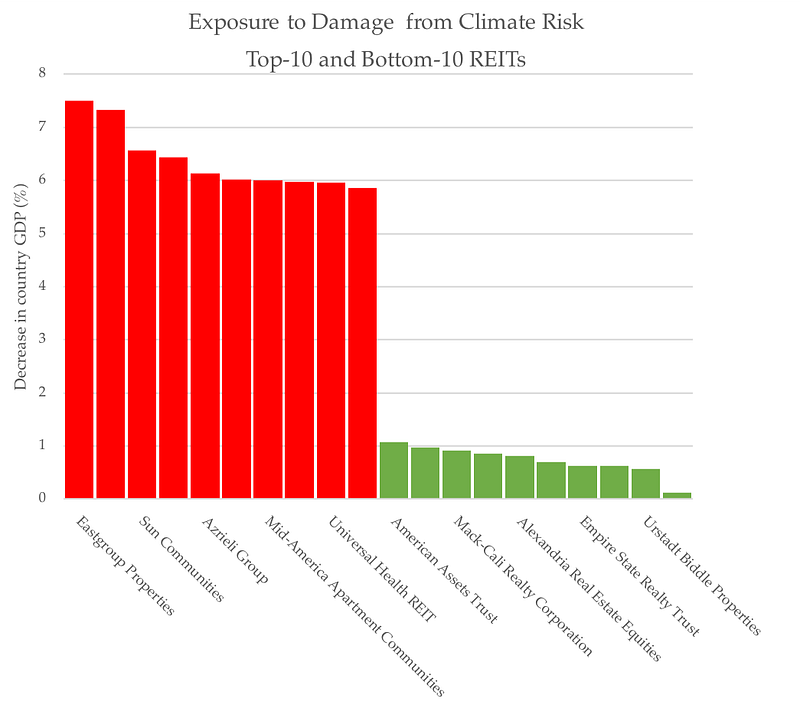

As a second climate risk layer, we use a forecast of total direct, financial climate damage as a percentage of county GDP. This data is based on recent research by The Climate Lab, published in the renowned Science journal. Using forecasts of changes in weather and climate (the medium IPCC scenario), this map shows the combined effect of these changes on agriculture, mortality, energy, low-risk labor, high-risk labor, coastal damages, property crime, and violent crime. Ultimately, this translates into a monetary effect on local GDP, as presented on the map.

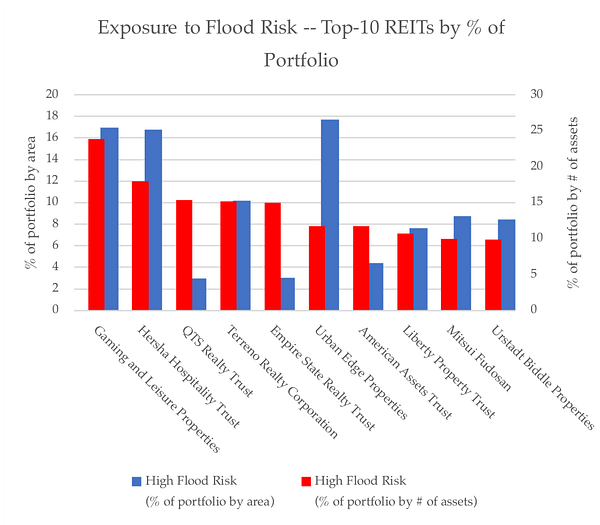

To get a better feel for how this affects real estate investors, we aggregate the data at the level of the REIT portfolio, both counting the number of buildings for each REIT portfolio that is exposed to flood risk and the broader measure of climate risk, as well as summing the total square footage of these buildings.

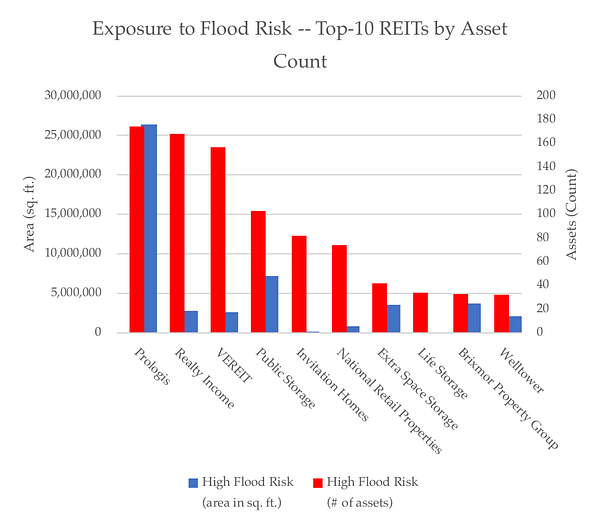

As it turns out, only 2 REITs are not affected by flood risk. The other 131 REITs are affected by flood risk— for these REITs, on average 87% of the portfolio measured by size (square footage) is exposed to at least some flood risk, as defined by FEMA. Looking at assets that are exposed to high risk, according to FEMA, about 5% of the average REIT portfolio is affected. That number may be small, but the value-at-risk is of course much higher. There is significant variation across REITs: Simon Property Group (SPG-N), the largest commercial real estate company in the world, has 85% of its portfolio in areas with low flood risk and 3% of its portfolio in areas with high flood risk, whereas 9% of assets in the Kilroy Realty Corporation (KRC) portfolio, one of the world’s “greenest” REITs, are exposed to high flood risk. The figures below below show the top-10 REITs by flood risk exposure, measured by asset count, and the top-10 REITs by flood risk exposure, measured by percentage of the portfolio.

As for climate risk, the data provides insight into the decrease in county GDP as a result of climate change — for each REIT, we calculate the exposure to such economic risk, by taking the average decrease in GDP across the counties where the REIT has assets. The figure below shows the top-10 and bottom-10 REITs by exposure to economic impact of climate risk.

Of course, “being exposed” to climate risk is not a big deal per se. It merely means that as a REIT, or as an investor in a REIT, you are more, or less, exposed to climate events, now and in the future. Depending on the extent of (private) insurance, a climate event, be it large or small, may not necessarily lead to material effects for the portfolio. But such thinking is short-sighted, which would not be prudent for an investor in a long-lived asset. Government insurance programs for climate events largely go unfunded. And insurance premiums can be adjusted annually. The average duration of a commercial real estate investment is 5–7 years, and often longer still. As the incidence and intensity of climate events increases, future buyers of an asset will start to take climate risk into consideration in underwriting and pricing of an asset — risk, or uncertainty, translates in higher return requirements, thus leading to a lower price for assets that are exposed.

Climate risk is, or should be, a non-partisan issue. Storms don’t recognize the political predisposition of an area, and neither does flooding. For (institutional) REIT investors, but also for investors in private equity real estate funds, or for direct investors in real estate, understanding exposure to any form of risk is paramount. The fiduciary duty of investors towards clients and trustees is the foundation of the capital market. Stewards of capital should carefully assess current and future risks. It’s time to add climate risk to the mix by using quantitative assessments of such risk, exploiting the insights that (big) data is increasingly bringing to the capital market.